High-Water Marks and Equalization: Why Manual Fee Calculation is a Compliance Minefield

Manual calculation of performance fees with high-water marks and equalization is a compliance risk. Spreadsheet-based fee logic is difficult to audit, prone to compounding errors across investor series, and frequently produces discrepancies that trigger investor disputes and regulatory scrutiny.

This article focuses on the compliance and fiduciary risks of manual fee calculation. For the step-by-step mechanics of HWM and equalization, see High-Water Mark Calculation and Equalization and the Free Ride Problem.

Why Is Manual Performance Fee Calculation a Compliance Risk?

For investment managers, the Performance Fee is often a major revenue driver. However, for those managing Alternative Investment Funds (AIFs) or Actively Managed Certificates (AMCs), calculating these fees is not a simple percentage of profits. For a full framework, see The Ultimate Guide to NAV Calculation.

The introduction of High-Water Marks (HWM) and Equalization logic transforms a routine accounting task into a high-stakes control area. When handled in spreadsheets, these calculations are more prone to errors that can lead to fee leakage, investor compensation issues, and, depending on jurisdiction and mandate, regulatory consequences.

What Makes High-Water Mark Calculation So Complex?

The High-Water Mark ensures that a manager only receives performance fees when the fund’s value exceeds its previous peak. While the concept is simple, the execution is not, especially when dealing with:

- Hurdle Rates: Fixed or floating benchmarks (e.g., SOFR + 2%) that must be surpassed before fees accrue.

- Crystallization Periods: Determining exactly when a fee is “earned” and moved from a liability to a payout (e.g., quarterly vs. annually).

For step-by-step mechanics, see High-Water Mark Calculation and Performance Fee Crystallization.

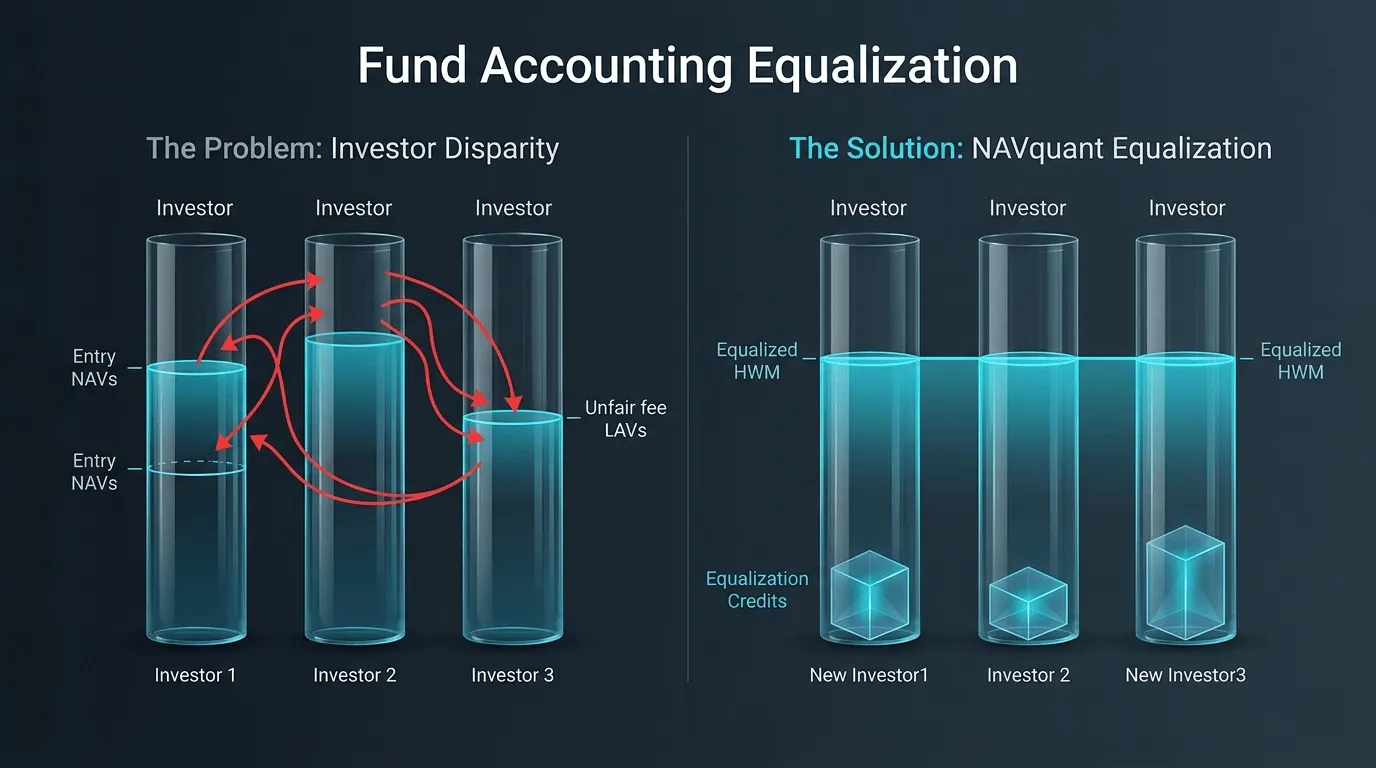

Why Is Equalization the Hardest Manual Calculation?

The most significant hurdle in manual NAV calculation is Equalization. When investors enter a fund at different times and different NAVs, a “free ride” problem can occur.

- The Problem: Assume Series A is down from 100 to 90. A new investor enters at 90, and NAV recovers to 100. Without equalization, that new investor may realize a +11.1% gain with little or no corresponding performance fee, while legacy investors are only back to breakeven and the manager’s fee allocation becomes economically distorted.

- The Solution: To ensure fairness, managers must use Series Accounting or Equalization Credits/Depreciation Deposits.

Managing these adjustments across hundreds of individual capital accounts in a spreadsheet is mathematically intensive and difficult to audit at scale. A single error in an equalization credit calculation can result in incorrect fee allocation for an entire series. For the full method comparison, see Equalization and the Free Ride Problem and The Building Blocks of Fund Fee Calculation.

How Does Manual Calculation Create Regulatory Exposure?

Regulators and auditors in major jurisdictions, including those supervised under frameworks involving FINMA or ESMA, scrutinize fee transparency closely. Exact obligations depend on fund structure and domicile, but manual “homegrown” systems often struggle to provide the granularity required during a forensic review.

The Risks of “Spreadsheet Logic” in Fee Accounting:

- Lack of Scalability: As the number of investors grows, the complexity of the equalization table grows exponentially.

- Non-Verifiable Calculations: Auditors may find it hard to trace the logic of nested spreadsheet formulas across multiple tabs.

- Investor Disputes: If a sophisticated institutional investor identifies a fee miscalculation, the resulting loss of trust is often irreparable.

How Does Automation Solve These Compliance Risks?

To mitigate these risks, many managers are moving away from manual workbooks toward automated engines like NAVquant.

By using a system-of-record that handles Equalization Credits, Series Accounting, and HWM resets natively, firms can improve:

- Accuracy: Automated logic reduces manual errors in fee crystallization.

- Transparency: A click-to-verify audit trail for every fee charged to every investor.

- Compliance: Adherence to the highest standards of fiduciary duty and regulatory reporting.