The Hidden Cost of Spreadsheets: Why Manual NAV Calculation is a Liability

Spreadsheet-based NAV calculation creates four structural risks that grow with fund complexity: formula decay that silently corrupts historical data, key-person dependency that concentrates operational knowledge, audit-trail deficits that fail regulatory scrutiny, and performance-fee leakage from manual high-water mark tracking errors.

What Are the Risks of Manual Fund Accounting?

In the early stages of a fund’s lifecycle, Excel is an indispensable ally. It is flexible, ubiquitous, and virtually free. However, as an investment manager scales, handling more frequent subscriptions, complex fee hurdles, or diverse asset classes, relying on manual fund accounting spreadsheets becomes a significant operational liability.

For Alternative Investment Funds (AIFs) and Actively Managed Certificates (AMCs), “spreadsheet-hell” is more than an inconvenience; it can become a structural risk to a firm’s fiduciary reputation and bottom line. For the broader context, start with The Ultimate Guide to NAV Calculation.

How Does Formula Decay Create Operational Risk?

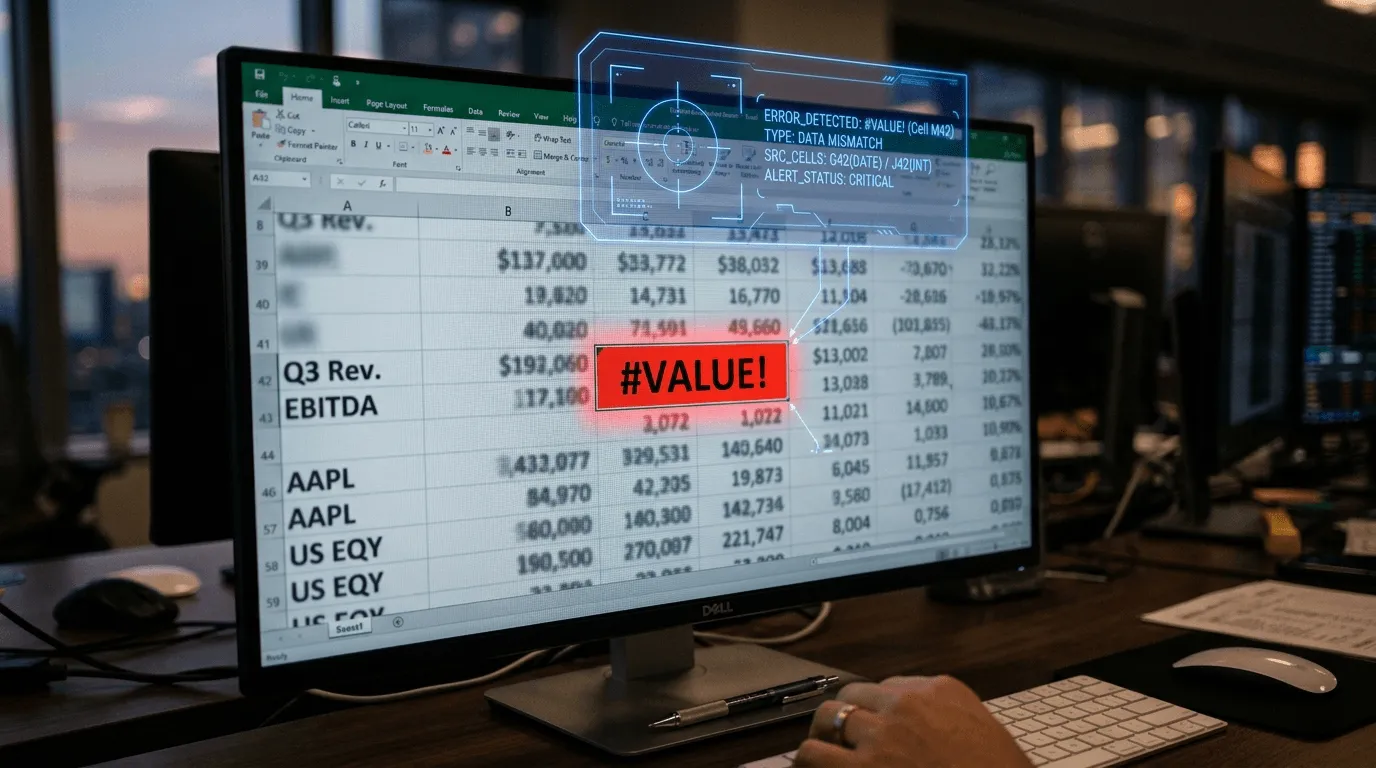

According to a European Spreadsheet Risks Interest Group (EuSpRIG) review of research literature, spreadsheet errors are present in an estimated 88% of production workbooks, with many containing material formula errors that persist undetected for extended periods. The primary risk of manual Net Asset Value (NAV) calculation is formula decay. In a complex workbook, a single hard-coded cell or an accidental reference change can ripple through historical data for long periods before detection.

Unlike dedicated NAV calculation software, Excel does not natively enforce many fund-specific integrity checks. A user can enter values that break internal accounting logic, increasing the probability of inaccurate reporting and potential regulatory or auditor challenge. For error impacts and thresholds, see NAV Errors and Restatements.

Why Is Key-Person Dependency a Critical Risk?

Many spreadsheet-based workflows are designed and maintained by a single individual. This creates a dangerous Key Person Risk. If the architect of the workbook is unavailable, the firm’s ability to report to investors or auditors can be materially disrupted.

Institutional investors conducting Operational Due Diligence (ODD) often view weak process redundancy as a red flag. They usually prefer managers who utilize standardized, multi-user platforms over bespoke “homegrown” workbooks.

Why Do Spreadsheets Fail Compliance Requirements?

Regulators and auditors increasingly demand granular transparency that manual systems struggle to provide consistently at scale. In a spreadsheet-driven process, the “how” and “why” behind a valuation change are often hard to reconstruct months later.

- Version Control Issues: It is difficult to prove exactly what data was used for a specific NAV pulse three months ago.

- Lack of Audit Logs: Spreadsheets do not record who changed a formula or when, making both internal fraud and honest errors nearly impossible to trace.

- Shadow Accounting Challenges: Without a clear system of record, performing shadow accounting to verify Third-Party Administrator (TPA) data becomes a manual, error-prone chore.

Why Does the Control Environment Matter More Than the Tool?

A spreadsheet can be workable for small, simple books, but what matters is the surrounding control environment. In practice, firms with resilient NAV processes enforce role-based approvals, reproducible calculation runs, and clear change histories. The stronger those controls, the lower the probability that minor input issues become published NAV errors.

This is why modernization is not only about replacing Excel. It is about building repeatable controls around data lineage, approvals, and reruns. For an implementation blueprint, see Automating NAV Calculation and The Audit-Ready NAV.

How Do Manual Processes Cause Performance Fee Leakage?

Accurately calculating Performance Fees and High-Water Marks (HWM) across multiple investor series is one of the areas where manual systems most frequently fail.

- Under-calculation: Results in lost revenue and lower fee income.

- Over-calculation: Leads to investor disputes, regulatory fines, and a total loss of trust.

Without a systematic approach to equalization and hurdle rates, the margin for error can grow rapidly with every new subscription. See High-Water Mark Calculation for the mechanics.

Beyond the Spreadsheet: Institutionalizing Your NAV Process

Transitioning from manual workflows to an automated, auditable platform like NAVquant is not just about saving time, it is about institutionalizing your operations.

By replacing “black-box” spreadsheets with a verifiable, cloud-based system, managers can provide auditors with a pristine trail of data and provide investors with the institutional-grade transparency they expect from a top-tier firm.